REITs: A Defensive HALO Against AI Obsolescence | May 2026

AI’s rapid evolution is producing substantial productivity gains, and we fully expect gains to continue. The expectation for exponential growth into perpetuity is driving volatility across the broader market, but, more importantly, we are seeing the early stages of a rotation into HALO asset classes (Heavy Assets, Low Obsolescence, introduced by Josh Brown on CNBC). This includes REITs and, as we will discuss, we expect this trend to accelerate as investors look to physical assets with durable cash flows.

–

On the other end, we should first concede that some AI fears are likely to prove true. Notably, the fear that AI agents could collapse entire industries, including software, have been severe enough to coin a new term: ‘SaaSpocalypse’. As a result, the iShares Expanded Tech Software ETF (NASDAQ: IGV) slid ~37% from its peak (9/23/25) to its trough (4/10/26). We are not software investors, but we see real risks that AI disruption could cause long term obsolescence for certain asset light business models. The risk that terminal value drops to zero is a stark contrast to real estate, and underpins today’s thesis that high quality REITs provide attractive defense for AI disruption.

–

Zooming out, an article penned by Citrini Research in February 2026 called ‘The 2028 Global Intelligence Crisis’ portrayed a dystopian scenario where AI replacement leads to a doom loop, pushing the unemployment rate above 10%. Importantly, Citrini expects job losses to focus on white-collar workers, which the market extrapolated to lower demand for office space, furthering fears around obsolescence risk in office buildings (already heightened). As of April 30th, office REITs, measured by the MSCI Office REIT Index (Bloomberg: RMSOFG Index), have produced a negative 5.3% total return YTD but troughed substantially lower on March 27th (nearly reaching -20%). Notably, office comprises a very small portion of the overall REIT universe (3.3% of the MSCI US REIT Index or RMZ), and the overall RMZ’s total return stands at 14.3% since the start of the year.

–

In general, we believe REITs’ physical asset bases and durable cash flow streams provide a bulwark amid uncertainty. REITs firmly fall into the HALO framework, which should be viewed a safe haven from AI disruption; tenants come and go, uses inside a building can change, but well-located real estate evolves and adapts. E-commerce was a sea change for society (“death of malls” was an inescapable refrain for decades), and certainly plenty of B and C malls no longer exist, but Simon Property Group’s (NYSE: SPG) ability to evolve alongside an adaptable real estate footprint drove an annualized total return of over 14% since 2000.

–

We don’t have a crystal ball, but fear mongering on potential disruption due to technological advancement is nothing new, and it historically has created buying opportunities for great businesses at low prices, and spawned entirely new industries. While we concede that total office utilization is at risk, we reiterate that office is a very small part of the REIT universe. Thus, we believe that the vast majority of the REIT index will be insulated, or even benefit from AI gains. Furthermore, the effect on office will be nuanced, as a ‘flight to quality’ could enhance values for well-located office buildings (and we think there are select opportunities for office outperformance). As we have said before, commercial real estate is a look-through to the entire US economy. As such, while the gains may be uneven, we feel confident that AI’s positive effects on the economy will flow through to most, if not all, commercial real estate sectors.

–

–

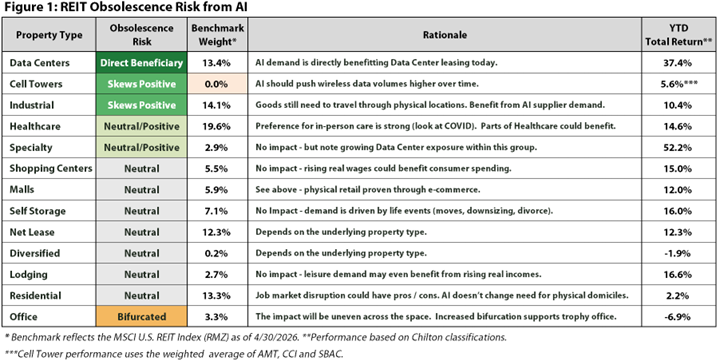

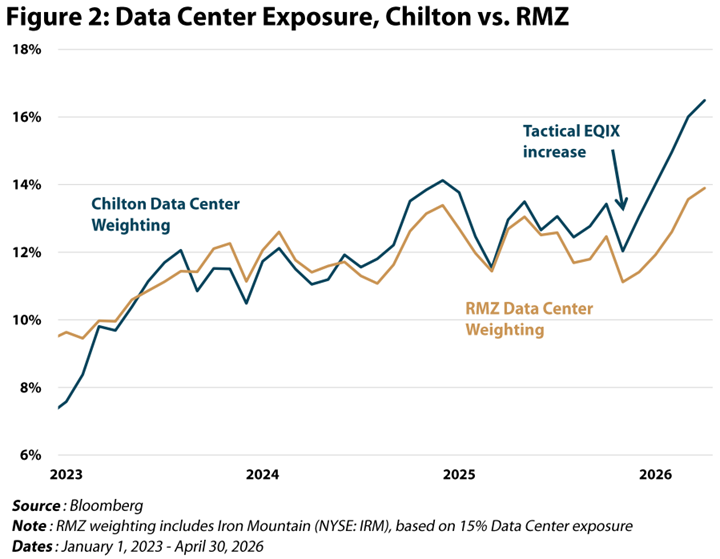

Figure 1 (on page 1) shows a summary of our thoughts on the impact of AI on each real estate sector. The primary direct beneficiary of AI is the data center sector, a ~260 bps overweight in the Chilton REIT Composite versus the RMZ (Figure 2). Overall, data centers, cell towers, and even industrial/healthcare (almost half of the RMZ – which does not include cell towers) could see benefits from AI’s rapid proliferation, and the vast majority of the remaining property types are neutral in our view.

–

–

Amid recent volatility, we are increasingly looking for names we believe have underappreciated AI exposure (such as Prologis Inc. (NYSE: PLD)) or who have been unfairly punished due to AI perceptions – thus far mainly adding to the pullback in high quality office names like BXP Inc. (NYSE: BXP) and Cousins Properties (NYSE: CUZ). There is another negative narrative that job losses will focus on younger cohorts, presenting a risk to owning apartment buildings. We see other reasons for caution in apartments today, but we are always monitoring the group for attractive entry points. Outside of these specific examples, our focus remains, as it always is, investing in low obsolescence, well-located real estate at an attractive basis, and thus the AI disruption is mostly a non-factor in our research process for sectors outside of data centers.

–

GDP Distribution Question

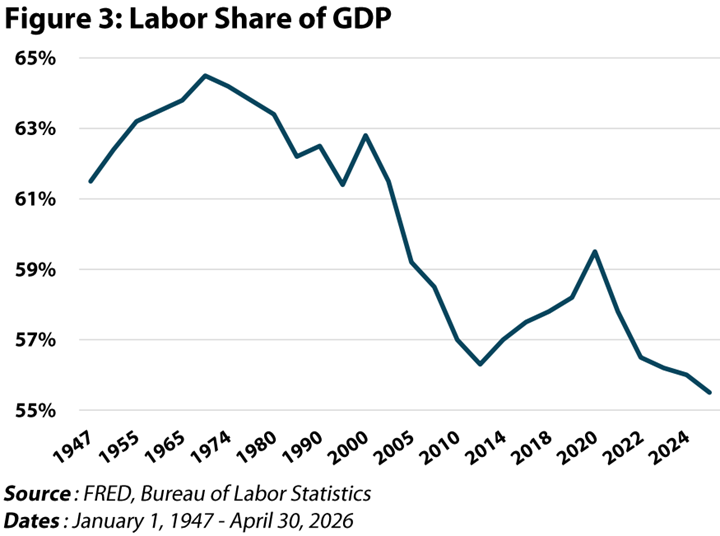

Ultimately, the doom loop thesis in the Citrini report hinges on expanded margins being recycled into more AI instead of labor, with labor’s share of GDP falling as a result. The notion that increased corporate profits become some sort of “Ghost GDP” doesn’t hold in our view. Output doesn’t vanish just because labor captures less of it. Labor’s share has been falling for decades while the economy grew (Figure 3). Capital owners spend and reinvest, firms redeploy savings (or return more to capital), and governments tax and redistribute.

–

–

No gains in human history have ever been evenly distributed, and, from a commercial real estate perspective, the distribution matters much less than the aggregate picture. A world of higher corporate earnings (even if it comes alongside lower payroll costs) provides firms with more capacity to pay rents and expand into new business lines. More importantly, these gains will still circulate through the economy. We can debate the relative propensity between labor, capital, and government, but we would never doubt America’s aggregate propensity to consume.

–

Is This Time Different?

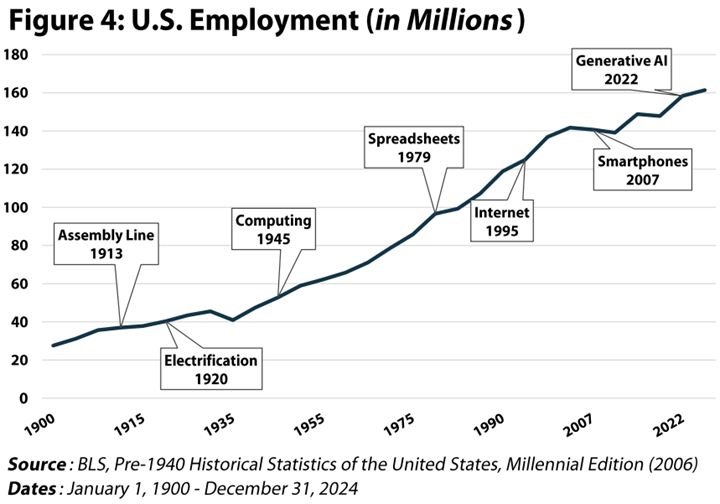

Figure 4 highlights over 100 years of employment in the United States, pushing through disruptions such as electrification, computing, the internet, and smartphones. At every inflection, there were fearful displacement warnings, but if we zoom out, one can see that overall employment continued to grow throughout. The historical pattern is clear, but the question is whether AI represents a break from history or a continuation.

–

–

There are real arguments worth addressing at this juncture. AI is more than a furtherance of automation; the current trajectory is increasingly targeting cognitive knowledge-based work. We believe two constants hold regardless of what type of work is automated. First, the demand for cognitive work is highly elastic. This held following the introduction of spreadsheets – when the cost of analysis falls, the threshold for what is worth analyzing also drops. The second factor to remember is accountability. AI cannot pass the bar, be a fiduciary, or sign an audit. Therefore, we agree that the pace of AI’s disruption could be different, but ultimately, the other side of any disruption will spur new jobs, businesses, and industries that will push growth more than offsetting any disruption.

–

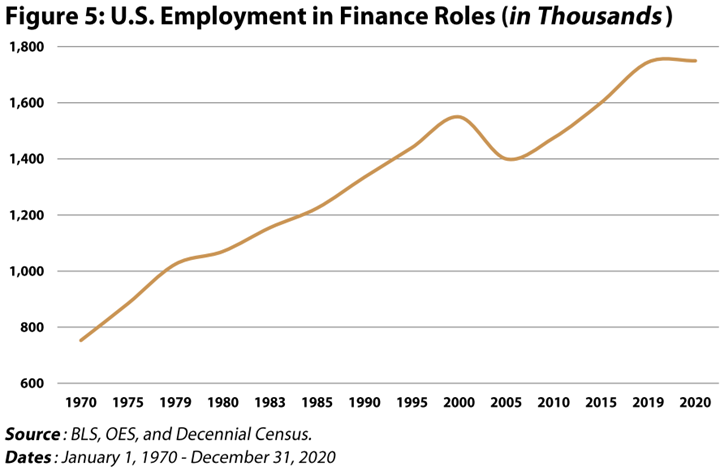

An example of a potential job-destroying technology advance was the ability to do spreadsheets on a computer. When VisiCalc launched in 1979 (Lotus 1-2-3 followed in 1983), consensus expected vast swaths of bookkeepers and junior analysts to be automated away. In reality, accounting and financial analyst employment (Figure 5) grew tremendously (e.g., lower analysis costs drove more analysis).

–

–

Defining Obsolescence

When lay investors or media discuss real estate obsolescence it is usually framed as a commentary on maintenance capex and, most notably, a judgement on the business inside the building. Rather, we view obsolescence as a function of an asset’s replaceability and adaptability. Replaceability asks if a competitor could build a substitute building that would serve the existing tenants the same or better; while adaptability simply judges how many different tenants and uses a building can support.

–

The best recent example is e-commerce and its impact on malls. As we noted above, plenty of poorly located and lower quality malls were forced into obsolescence, but the best properties and operators were able to evolve (splitting anchors, focusing on experiential tenants, etc.), and ultimately took market share from weaker players. Another example to consider is the proliferation of automobiles and the resulting exodus of residents from urban cores. Manhattan never surpassed the peak population set in 1910 (2.33 million), but the city’s proximity to business and education centers positioned it to not only survive but thrive in a changing world.

–

We believe replacement costs present additional protection against obsolescence. More specifically, we do not expect AI to lower the cost of construction. Therefore, new supply (in any property type) would be non-existent unless rental rates rise to justify new construction.

–

Case Study: 343 Madison

Last summer, BXP unveiled plans to develop a class A+ trophy office tower at 343 Madison Avenue, including direct Grand Central Terminal access via a dedicated easement. This passes replaceability with flying colors – even with unlimited capital, no competing developer can recreate this access. On adaptability, we concede that market office rents in Midtown Manhattan would not support a conversion away from office, but the depth of firms seeking the network effects of Midtown Manhattan and ease of direct terminal access is boundless. In other words, when replaceability approaches its upper limit, adaptability becomes a secondary concern. Consider 60 Hudson Street’s analogy, purpose built in 1928 as Western Union’s operation center, which should have been rendered useless when the telegraph became obsolete. Instead, the building’s irreplaceable connections to crucial fiber networks made it one of the most valuable data centers in the world.

–

Readers might expect AI concerns caused corporate tenants to pump the brakes on office leasing. Quite the contrary, the latter parts of 2025 and thus far into 2026 have seen active leasing environments. For BXP, we point out that 343 Madison is already ~30% pre-leased with Starr Insurance agreeing to take 275,000 sq. ft. through the end of 2049. This is a sophisticated tenant (with better visibility into AI’s productivity potential than most) signing a very long dated commitment for space.

–

Commodity Property Risk

We argue that the most likely outcome of AI-driven disruption is that it will accelerate the bifurcation we are already seeing in the office market. Specifically, as firms rationalize real estate footprints, we expect consolidation into fewer, higher quality locations. ‘Tip of the spear’ assets will not just survive disruption; more bifurcation means they will capture a disproportionate share of the remaining demand.

–

Do not take our arguments to mean all real estate is immune from obsolescence – suburban commodity office buildings will certainly suffer, just as lower end malls did. However, this trend has been underway for decades. Analogous to the acceleration in trends caused by COVID, AI could pull forward some obsolescence, but we do not believe the properties that have remained relevant (and thrived!) face new obsolescence risk. The concentration of trophy and class A properties held by REITs is no accident, and these companies should be rewarded for ‘paying up’ (accepting lower near-term returns) for lower obsolescence risk.

–

Terminal Value

Consider a final asymmetric distinction for REITs. The terminal value of a software (or other asset light) company whose product is displaced by AI could plausibly approach zero. Netscape Navigator enjoyed 95% browser share in 1995 but was functionally eliminated by the early 2000s, and AOL peaked at a market cap of $222 billion in 1999 before eventually being sold for $4.4 billion, a 98% decline. However, the terminal value of irreplaceable real estate is anchored in physical scarcity that no technology cycle has ever eliminated. Land that cannot be recreated, access that cannot be replicated, and buildings that adapt across uses stand the test of time regardless of which tenant is writing the rent check. Therefore, we do not view AI as a thesis breaking disruption for well positioned REITs; rather we expect AI to further the bifurcation trend underway in many property types and more likely drive benefits through higher household wealth.

–

Thomas P. Murphy, CFA

tmurphy@chiltoncapital.com

(713) 243-3211

Matthew R. Werner, CFA

mwerner@chiltoncapital.com

(713) 243- 3234

Bruce G. Garrison, CFA

bgarrison@chiltoncapital.com

(713) 243-3233

Isaac A. Shrand, CFA

ishrand@chiltoncapital.com

(713) 243-3219

–

RMS: 3,490 (4.30.2026) vs. 3,054 (12.31.2025) vs. 3,177 (12.31.2021) vs. 1,433 (3.23.2020)

–

An investment cannot be made directly in an index. The funds consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use.)

The information contained herein should be considered to be current only as of the date indicated, and we do not undertake any obligation to update the information contained herein in light of later circumstances or events. This publication may contain forward-looking statements and projections that are based on the current beliefs and assumptions of Chilton Capital Management and on information currently available that we believe to be reasonable, however, such statements necessarily involve risks, uncertainties and assumptions, and prospective investors may not put undue reliance on any of these statements. This communication is provided for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any Chilton investment or any other security. Past performance does not guarantee future results.

Information contained herein is derived from and based upon data licensed from one or more unaffiliated third parties, such as Bloomberg L.P. The data contained herein is not guaranteed as to its accuracy or completeness and no warranties are made with respect to results obtained from its use. While every effort is made to provide reports free from errors, they are derived from data received from one or more third parties and, as a result, complete accuracy cannot be guaranteed.

Index and ETF performances [MSCI and VNQ and FNER and LBUSTRUU] are presented as a benchmark for reference only and does not imply any portfolio will achieve similar returns, volatility or any characteristics similar to any actual portfolio. The composition of a benchmark index may not reflect the manner in which any is constructed in relation to expected or achieved returns, investment holdings, sectors, correlations, concentrations or tracking error targets, all of which are subject to change over time.