Portfolio Insight | 1st Quarter 2026

The stock market reached a new all-time high on January 27th as hopes for strong corporate earnings, slowing inflation growth, and interest rate cuts buoyed investor sentiment. However, February saw the beginning of weakness driven by renewed AI and private credit concerns as well as increasing tensions in Iran that boiled over into a full-blown war on February 28th. From there, volatility spiked, equity markets came under pressure, and the S&P 500 closed the first quarter down 4.4%.

Sector returns diverged widely in the period. The strongest sectors were Energy, Materials, and Utilities while Financials, Consumer Discretionary, and Information Technology trailed the most. The majority of mega-cap growth stocks faltered, and value names registered significant relative outperformance in the period.

Apocalypse or TACO

With the Iran war introducing unexpected risks, the market rightfully pulled back into the end of the quarter. Unclear objectives, an unpredictable and formidable adversary, spiking energy prices, and President Trump’s usual aggressive rhetoric will likely keep volatility high until the conflict ends and commodity shipments through the Strait of Hormuz resume. Roughly 20% of global oil supply, along with significant volumes of fertilizers and industrial gases, flows daily through the waterway. The longer it remains closed, the greater the risk to global economic growth, particularly in Asia and Europe, which rely more heavily on imported oil due to limited domestic production.

In the meantime, the market is on edge, not sure whether to position for Apocalypse or the “Trump Always Chickens Out” (TACO) trade. President Trump wants to be tough but probably has a pain threshold when it comes to market declines and possible significant Republican losses in midterm elections. The path to peace and lower oil prices is uncertain, but a quick deescalation or resolution by Trump could drive markets sharply higher. So, it is arguably ill-advised for equity investors to be too bearish or too bullish at this time.

Shifting Market Leadership

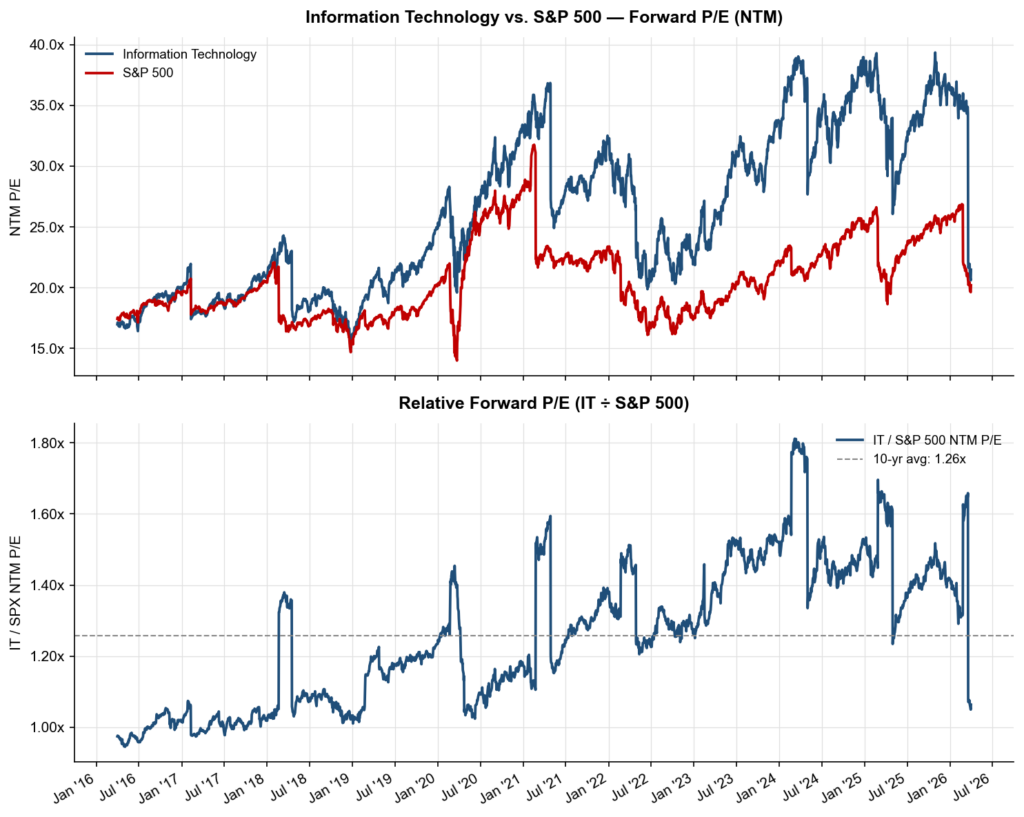

Even before the March volatility spike, investors were again questioning the AI infrastructure buildout and seeking more defensive names amidst increasing uncertainty. In particular, value stocks in sectors like Energy and Materials were significantly outperforming growth names in areas like Information Technology and Communication Services. Additionally, the equal weight S&P 500 was outperforming the market cap weighted S&P 500 index.

However, as with other short periods of leadership change and broadening in recent years, it is currently unclear how long current trends will last. The valuation of technology stocks has become particularly attractive. Many of these companies retain a very strong multi-year earnings outlook relative to the rest of the market, even as their stocks are being hit with severe multiple contraction. When the expected coming growth materializes, growth sectors like tech will be poised for a major rebound.

Source: Bloomberg, Chilton Capital Management

Recalibrating Market Expectations

Entering 2026, catalysts for new market highs included robust earnings growth (led largely by AI spending), lower inflation growth, interest rate cuts, and a relatively stable geopolitical environment. The earnings outlook was shaping up to be even better than initially expected for the next several years, and the S&P 500 hit a new all-time high in late January.

However, the surprise attack on Iran by the US and Israel, and the ensuing war caused the price of oil to spike over 50% and pushed interest rates higher amid renewed inflation fears and economic uncertainty. Downside risks to the economy and market have increased.

Domestic Equity Outlook

Due to these negative developments, a more tempered outlook for full year 2026 market returns is warranted. Once a favorable resolution to the Iran war is reached, we expect markets to bounce back from current oversold conditions due to the continued strong overall earnings outlook. However, timing is uncertain, and a lower valuation multiple should be applied due to the expectation for higher inflation and interest rates. So, for the year, a mid-single-digit return currently seems more likely than the previous outlook for a high-single-digit return. This would still represent a greater than 9% gain from quarter-end.

As usual, Chilton equity portfolios are well balanced, and as active managers we are able to pivot quickly should market conditions change materially. So far, significant modifications are not necessary. However, the investment team has been highly active in researching new ideas. Major themes like AI, power, defense/aerospace, and improving capital markets activity are attractive areas for investment. Our team has used recent market volatility to upgrade portfolios with several new stocks.

Fixed Income Outlook

Like the S&P 500, the bond market moved lower in the first quarter, due to both higher interest rates and a widening of credit spreads. The Bloomberg US Aggregate Bond Index, a mix of government and corporate bonds, fell 0.1%. The 10-year Treasury yield rose from 4.18% at the beginning of the year to 4.30% by quarter-end, while 2-year Treasuries, which are more influenced by current and expected future Federal Reserve policy, moved from 3.47% to 3.79%.

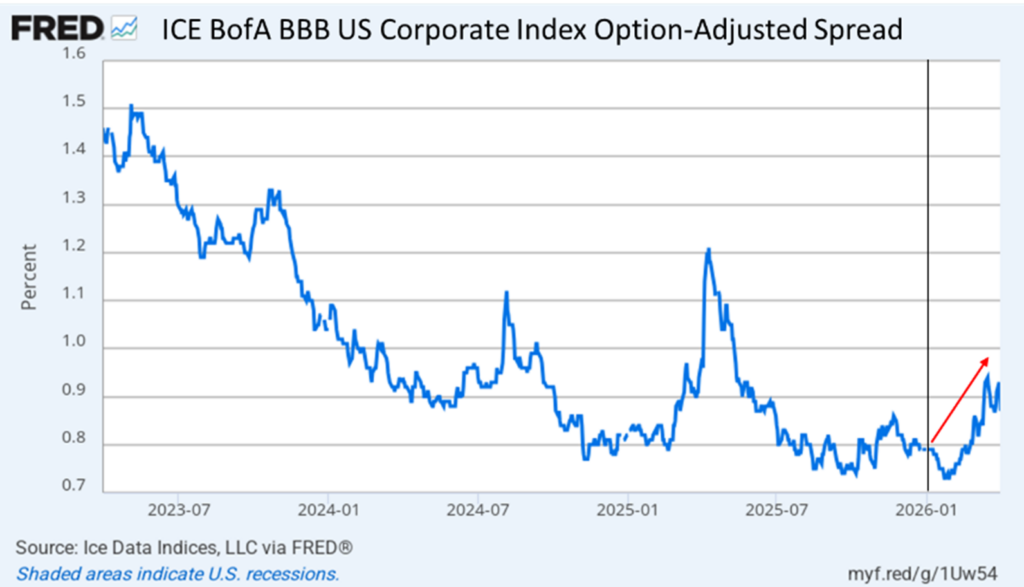

The rise in interest rates is directly correlated with the conflict in Iran. More specifically, the spike in energy prices globally has increased the likelihood of higher inflation in the coming months. As a result, instead of the Federal Reserve cutting short-term interest rates in 2026, the Fed is now highly likely to leave rates unchanged for the foreseeable future. The significant increase in energy prices has also increased the potential for a recession, especially if the conflict drags on. Recessionary concerns have begun to show up in credit spreads (the incremental yield of a corporate bond over an equivalent-term risk free, i.e. Treasury, investment). Credit spreads tend to be a good leading indicator of economic trouble, although they remain well below average compared to the last several years.

Source: St. Louis Federal Reserve

Presumptive new Federal Reserve Chairman Kevin Warsh, handpicked by President Trump, will enter his new position in a time of significant uncertainty. Although Chairman Warsh still needs to be formally confirmed by the Senate, navigating monetary policy in the face of this energy shock will be a significant challenge. Building a consensus on the committee is further complicated by President Trump’s vocal push for lower interest rates. Markets are likely to react unfavorably if the Fed’s independence is called into question. In this case, the fear that stimulative short-term rate cuts might trigger longer-term inflation would likely push rates even higher. The upshot of the recent decline in bond prices is that yields for bonds bought today are more attractive. At year-end, a significant percentage of bonds in client accounts yielded less than 4%. Today, most bonds we have been buying, with maturities of 1-7 years, yield between 4.25% and 4.75%. As always, bonds purchased for most client accounts are investment-grade quality and are bought with the intention of being held until maturity.

Global Markets Outlook

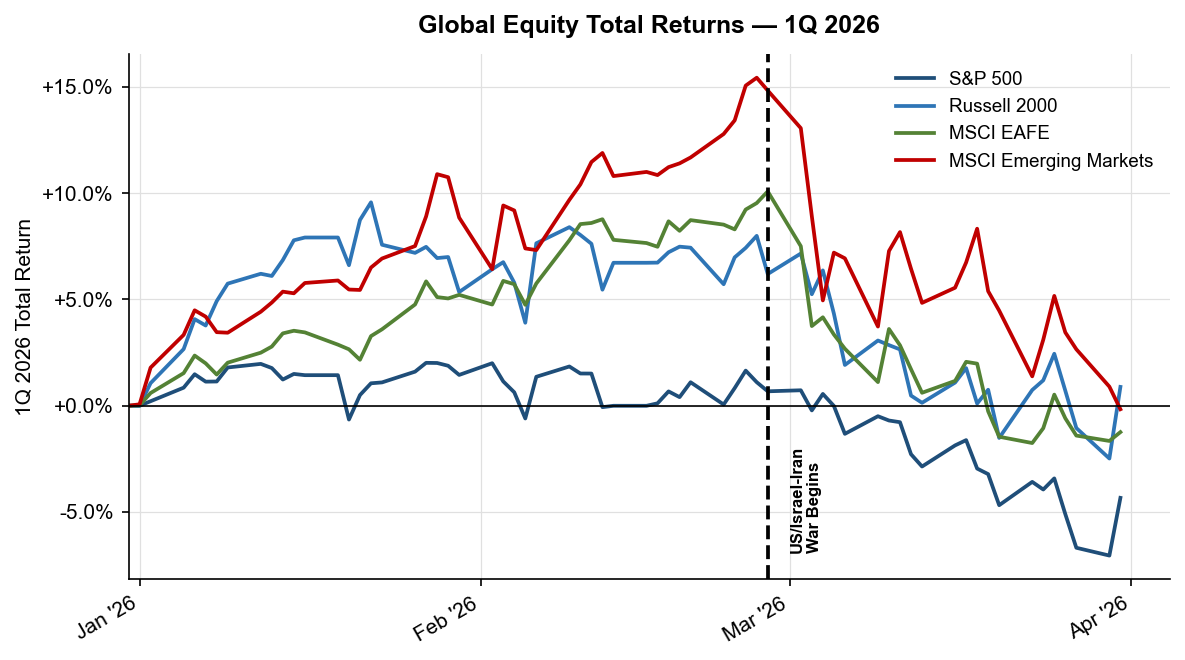

Global equity markets largely retreated in the first quarter of 2026, with one notable exception. After posting solid gains earlier in the quarter, emerging markets and international developed markets gave back those advances as the Iran war escalated late in the period, ending down 0.1% and 1.1%, respectively. By contrast, US equity performance was more mixed: small caps were the only major equity class to finish in positive territory, rising 0.9%, while large caps declined 4.4%.

Source: Bloomberg, Chilton Capital Management

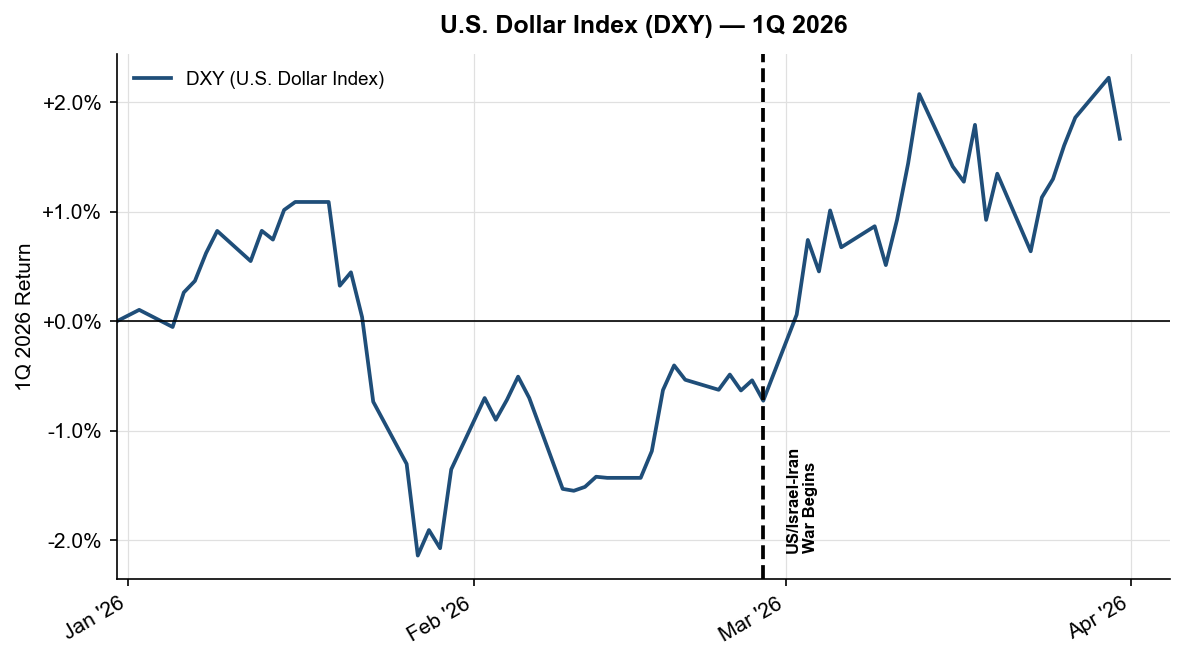

While the US lagged for most of the first quarter, it has outperformed since the war with Iran began. Part of that relative strength reflects a move back toward traditional safe havens, including the US dollar. The US Dollar Index (DXY) has risen 2.4% since the start of the conflict, reinforcing its standing as the world’s de facto reserve currency at a time when many investors had begun to question it.

Source: Bloomberg, Chilton Capital Management

From an investment standpoint, several existing themes have continued to drive returns. The AI trade has broadened to benefit markets such as China, Taiwan, and South Korea. National defense has also remained a strong theme as heightened security risks and heavy munitions usage support the need for additional production. By contrast, software has remained under pressure amid concerns about AI-driven disruption.

International markets have also benefited from their heavier exposure to value stocks. Rising commodity prices have supported value-oriented sectors, while weakness in software has weighed on growth. Even so, international markets remain more vulnerable to higher energy costs because Europe and Asia are more dependent on imported oil and LNG, while the US remains a major energy producer. In periods of heightened uncertainty, that advantage, combined with a broader flight to quality, tends to support US assets. Looking ahead, near-term performance will likely remain tied to developments in the war, while longer-term returns should be driven by earnings growth relative to expectations. With the path of the conflict still uncertain, global diversification remains a prudent strategy for many investors.

REIT Commentary

In the first quarter of 2026, the MSCI US REIT Index (RMZ) produced a total return of +4.8%. It was an extremely volatile quarter, which peaked with the RMZ up over 11.8% through March 2, only to fall 6.2% in the remainder of the quarter given the potential for higher inflation and interest rates following the initial attack on Iran.

The big news in REITland in March was the announcement of an all-stock merger between Public Storage (NYSE: PSA) and National Storage Affiliates (NYSE: NSA) where PSA is acquiring NSA for a $10.7 billion enterprise value. This came soon after the announcement of an all-cash acquisition of Veris Residential (NYSE: VRE) for $3.4 billion. While mergers and acquisitions (M&A) are notoriously difficult to predict, 2026 is off to a hot start, and we are hopeful that more REIT management teams and boards of directors will pursue M&A to get the best outcome for shareholders.

We believe the sector is ripe for M&A today due to: 1) discounts to net asset value (NAV), 2) increasing NAVs, 3) expectations for eventual rate cuts by the Federal Reserve, 4) low obsolescence risk, and 5) rising replacement costs.

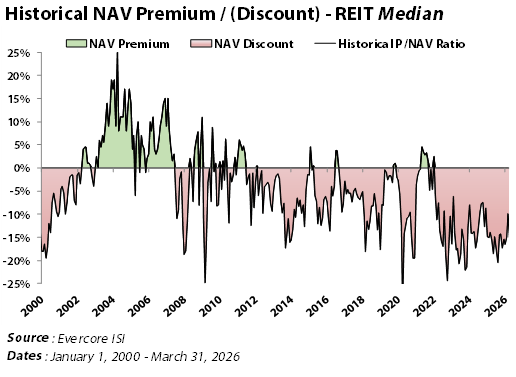

As of March 31, 2026, the median REIT trades at a 15% discount to NAV, and the 86 public REITs we cover range from a 55% discount to an 87% premium. In fact, public REITs have traded at a discount on roughly 88% of trading days in the past 16 years! The persistent discount over the past decade reflects three main forces. First, the rise of passive ETFs has driven indiscriminate buying and selling based on index weights, reducing the impact of active REIT investors who once targeted discounted companies and helped close NAV gaps. Second, generalists place less emphasis on NAV, and with REITs viewed as value and mid-cap stocks—both recently out of favor—interest has remained muted; real estate was still the most underweighted sector in Bank of America’s March 2026 Investor Survey. Third, revived non-traded REITs and private real estate absorbed capital that might otherwise have flowed to public REITs.

We are tracking five different REIT activist campaigns, and eight REITs are already in liquidation or pursuing strategic alternatives. Although 2025 only had ~$6 billion in REIT M&A, we believe that at least ~$45 billion will close in 2026 merely based on what has been announced. In a time of volatility and unpredictability, active managers such as ourselves can produce alpha by including M&A targets in the portfolio. We have two currently, which we believe will be resolved this year. We continue to find good opportunities in the market volatility and are hopeful that REIT management teams will act in the best interests of shareholders.

Bradley J. Eixmann, CFA

Brandon J. Frank

Robert J. Greenberg, CFA

Matthew R. Werner, CFA